Concerns over the Supply Chain? We’ve got your back!

We’ve teamed up with our family of brands to bring you our Supply Chain Support Center. This center will be the best place for you every week to stay up to date on all things supply chain!

Market Alerts & Produce Updates

For the week of April 29, 2024

The following updates and alerts were culled in collaboration with our growing family of brands. Scroll through both lists to help prepare for upcoming obstacles and opportunities.

Grain Due to favorable planting conditions in the US, strong harvest reports from South America, and rising soybean oil supplies, soybean oil futures saw an almost 5% decrease last week. Canola futures in California decreased in tandem with the price of soybean oil, and exports are minimal. Because soy prices are rising, palm is finally losing ground.

Dairy The market for shell eggs is collapsing, and demand has decreased. Over the last four weeks, cage-free supply have increased by 22.2%, despite the avian virus causing major production interruptions. Block and barrel sales are steadily rising. Producers of butter report a decline in sales of both salted and unsalted butter.

Beef As long as buyers use caution and keep their buying windows closed, tenders and ribs will remain tender, with equally applied pressure to both butts and strips. Buyer pressure on bids continues to impact chucks, insides, and end cuts. With the growing harvest, there seems to be less of a drive for lean meats. Grains are still mixed because of a fluctuating supply and a predicted increase in demand.

Pork Butts are still rising more quickly than expected. As the holiday draws nearer, the demand for butts is only going to rise. Because of the current slow demand, ribs will be flat next week. Strong exports and retail interest are driving up loins as well. Bellies are still in high demand, and the market is still unstable.

Poultry This week, breasts leveled out. The demand for wings has increased. There is a high demand for tenders, yet they are still the hardest to locate offering. The desire for dark meat is still high. The majority of whole birds are balanced.

Seafood Prices have increased despite food service revenues being steady during the Lenten season due to rising labor, energy, and other operational costs. It will be difficult to maintain sales throughout the year as a result. Shrimp sales are projected to be stimulated by the anticipated summer demand rise following Lent.

All wet veg items will be shipping from the Salinas Valley as supplies increase and quality improves. As mentioned previously, due to the abundant rainfall in California, farmers are witnessing a rise in anthracnose, a fungal infection that has resulted in reduced yields of iceberg and romaine lettuce. As a precautionary measure, harvesting teams are trimming the products to alleviate these concerns, resulting in lighter case weights than usual. Overall most commodities are seeing a decline in markets. However, the romaine and iceberg markets remain higher due to quality issues. The avocado inventory in the US is significant, and Cinco pulls are commencing. Due to recent market volatility, strong Cinco promotions are not as guaranteed as during the Super Bowl.

Artichokes We continue to see a limited supply of artichokes. 18ct – small loose artichokes are very tight as Oxnard is done and Salinas has started in a light way with low volume, only producing large sizes (12ct.) Expect smaller sizes to be very tight for the next several weeks.

Asparagus Asparagus production has dropped due to seasonality from Caborca & San Luis, Mexico. Obregon, Mexico has started with low production. Peru continues to increase production. Markets remain the same. White asparagus continues to be very limited to non-existent from Peru.

Avocado Last week's harvest closed at 68.5M pounds, up 9% from the previous week. Projections for this week call for 58M pounds, and current harvest levels support that figure. Markets have moved up considerably on larger-sized fruit. The size curve continues to shift to smaller-sized fruit. The normal crop continues to mature, with dry matter averaging 35%, ripe cycles are shorter, and fruit is at a peak eating experience.

Bananas Steady supply and quality remain good.

Blueberries Blackberry production continues to be relatively steady and newer varieties are yielding good numbers, keeping supply steady. Quality is good, with sizing between the medium to large range, a nice sheen, mostly black, and good firmness. Due to high temperatures in the regions, we will see some regression in some ranches and softer fruit as the days get hotter. Moving into the next few months, supplies are anticipated to remain lower.

Broccoli Salinas broccoli volumes have improved, and the market has adjusted down. Supplies look steady going into next week with very good quality.

Brussels Sprouts Overall supplies and quality remain good as Mexico and the Oxnard growing regions are in full production. Supplies are heavy to Mediums with Jumbos and Smalls in short supply.

Cabbage, Red Quality is good although supplies continue lighter. Market is steady.

Cantaloupe Steady volume on offshore fruit, peaking on 9/9Js with a limited number of 12/15s coming in, but enough to cover all contracted needs. The quality of the cantaloupe remains at optimum levels with excellent color and some of the best eating fruit we have witnessed all season. Brix levels remain consistently in the 13-16% range. Carton weights are also increasing as seed cavities get smaller and brix levels go up. There is also local cantaloupe available out of Florida this week.

Carrots Steady supplies continue with good Quality. Shippers still have light volume on Jumbos out of California.

Cauliflower We have seen a significant decrease in supplies due to planting delays from previous cool wet weather during planting season, Quality remains good.

Celery The market continues to trend higher as supplies are anticipated to decrease over the next few weeks.

Cilantro Cilantro supplies, and Quality continue to improve.

Corn Good supply available out of Florida and Mexico this week. Quality is good out of the southeast and South Georgia projected to start the 2nd week of May.

Cucumber Steady supply available out of McAllen, Nogales, and Florida. South Georgia is projected to scratch on new crop at the end of April.

Grapes, Green/Red Grape availability is slowly improving but we do expect elevated pricing through the first part of next month. We are starting to see a bit more availability from Mexico on both coasts which is putting downward pressure on the market. We hope to see this trend continue over the next 3 weeks. Quality is fair and we are still asking for subs to black grapes since they seem to have the best quality and legs over the red and greens.

Herbs Basil quality continues to improve each week. We are still seeing some quality issues with dill.

Lemons We are seeing a significant size shift on Lemons. Small fruit is getting exceptionally short with reports that 70- 80% of the crop is running 95’s/115’s/140’s with no relief in sight until imports start in late June.

Lettuce, Boston/Butter/Green/Red Leaf Production in Salinas Valley is steady. Overall quality is good. Current markets are steady with good demand.

Lettuce, Iceberg Lettuce supplies are still slightly below normal as the fields are growing slowly due to cooler weather, with head size and weights lighter than normal. Overall quality is good, but solidity is slightly softer due to the slow growth. The market is steady at current levels.

Lettuce, Romaine Romaine and Romaine Hearts are steady and overall quality is good to fair. Current markets for Romaine and Romaine Hearts are very active with strong demand and look to remain strong for approximately the next three weeks. Some growing areas in the Salinas Valley are experiencing some pressure from Anthracnose from the rains during the growing cycle, which is affecting quality from some shippers.

Limes Overall demand is improving and the market is strengthening as we approach Cinco de Mayo and pricing will remain firm. We continue to see increased crossings on small sizes; large sizes will become more limited in supply. Due to lack of rain, scarcity of large fruit could be extended, and pricing may even climb. 110's & 150's are in extremely short supply to almost non-existent market wide.

Mushrooms Stable supply and good quality available.

Onions, Green We continue to see better supplies out of Mexico, although the market remains at higher-than-normal levels. Quality is improving.

Peppers, Green Better supply this week across all sizes and Quality is good. The desert is expected to start in May with South Georgia scratching late April.

Peppers, Red Excellent supply and good quality available on all sizes.

Pineapple Steady supply and quality remain good.

Potatoes, Russet The market continues to feel stable on all sizes and grades for the moment, with the exception of 40ct potatoes. While potatoes as a whole should remain plentiful, we do anticipate 40ct commanding a premium more often than not until the end of the crop. They have continued to be available for mixers, but we are not seeing very much straight load availability, or even availability in heavy volume. There will be some lots that are better than others throughout the season, but this does appear to be a theme moving forward. Because of this, we do anticipate that we may see a pretty big gap between 40ct/50ct and the rest of the sizes. The good news is that food service sized cartons in the middle size range (60/70/80) appear to be plentiful.

Spinach Supplies are good, Quality is fair due to some of the cool, rainy conditions that the Salinas Valley experienced over the winter.

Squash, Yellow/Zucchini Shipping out of Florida, McAllen, and Nogales. Good supply and Quality available in general. Best Quality continues to be on zucchini while yellow squash, with its tender skin far more vulnerable to imperfections, seems to remain very light in supply. South Georgia is about 2 weeks from scratching.

Strawberries There is a positive outlook for the upcoming increase in strawberry production as we anticipate the adverse weather conditions to subside next week. The strawberry plants are thriving and strong and we expect a substantial yield in the following weeks. While there may be a need for some cleanup due to rain damage, we remain optimistic about the significant boost in production for Santa Maria and Watsonville. Although we have noticed some fruit with minor imperfections such as misshapen button nose tips, green shoulders, and pinrot in the fields, harvest crews are effectively maintaining cleanliness during the packing process.

Tomatoes, Cherry Crops out of Mexico are slowly improving and we are seeing a downward trend on price as the volume increases. Unfortunately, with the imbalance on the east coast due to less acreage planted and weather-related pressure, markets remain at record highs. We will see this continue until Florida can produce volume consistently.

Tomatoes, Grape Out of the east, good supply and quality are available. Out of the west, steady supply and good Quality are available, crossing through McAllen and Nogales.

Tomatoes, Roma Markets remain unstable with good volume available this week. Quality is much better this week. Out of Mexico, good supply and Quality available this week. We expect volatility in the roma market over the next 3 weeks.

California Weather Alert

December 13, 2022 – The West Coast and San Joaquin Valley of California, has been receiving rainfall over the last few days, impacting all growing areas including Salinas, Santa Maria, Oxnard, into southern California and the Central Valley.

As a result, this has caused delays as fields are too muddy to harvest. Unfortunately, there has not been enough rain to reverse the major drought conditions they continue to experiencing, but is enough to affect harvesting for a few days.

Comments or Questions?

Schedule a meeting to connect directly with a Supply Chain Expert from the Buyers Edge Team.

The Buyers Edge Platform has been busy putting together all of the insights you need around the strained supply chain. Sign up for one of our upcoming webinars, read some expert insight, or check out our collection of Market Report blogs below!

Sign up for our Monthly Supply Chain Newsletter to get these insights delivered to your inbox

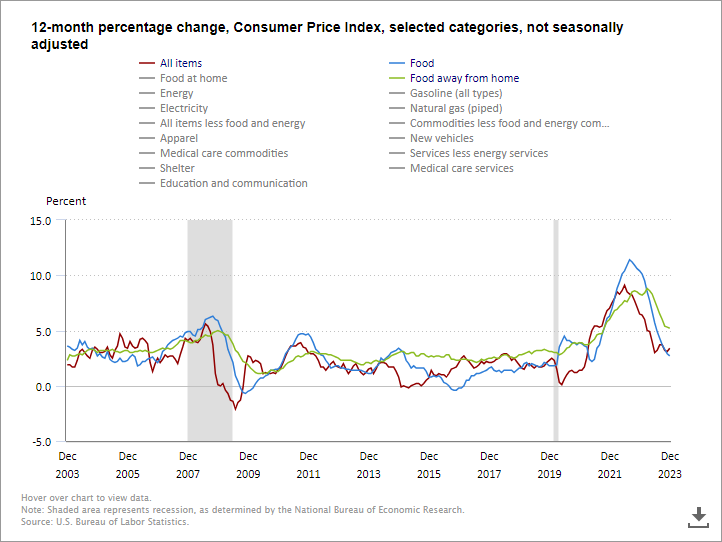

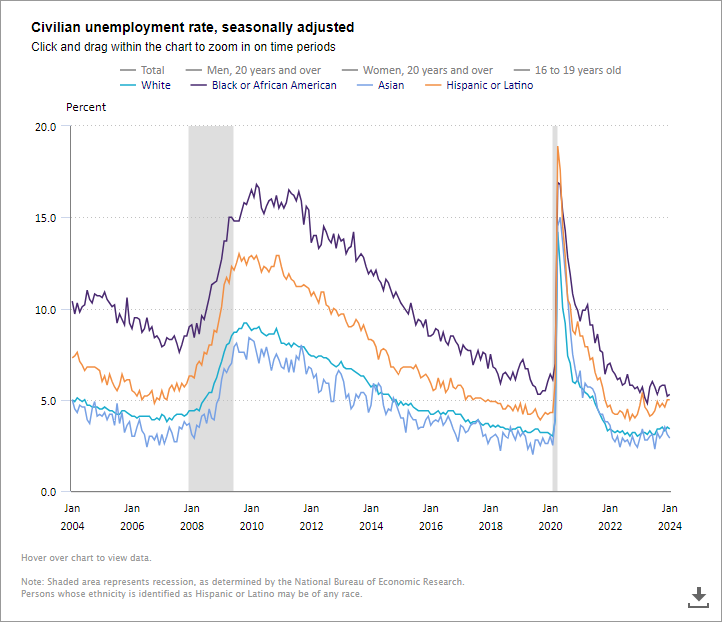

The Latest Facts & Figures

Live charting from industry experts

Monthly Economic Research From Our Partner:

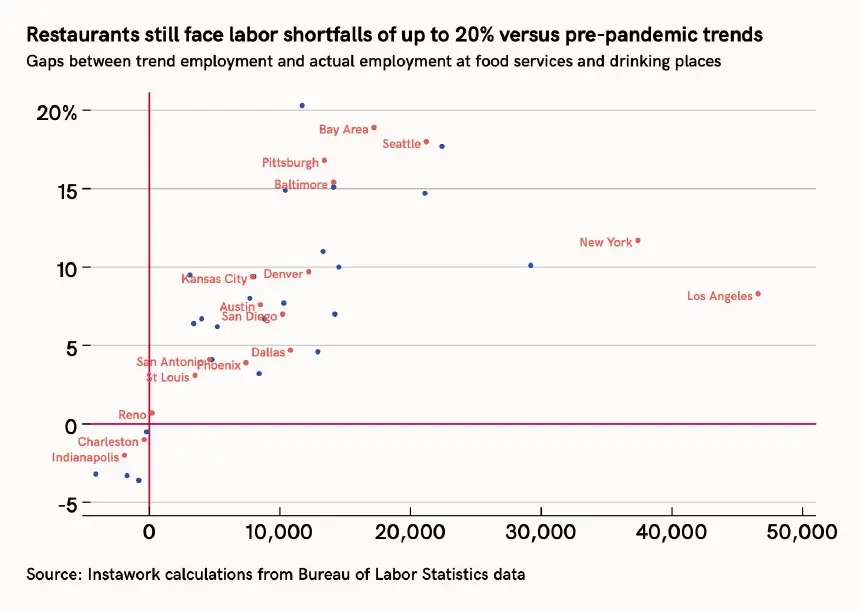

Where are labor shortfalls worst?

Though employment in hospitality has largely returned to pre-pandemic levels, a growing economy means labor shortfalls continue. Adjusted for inflation, spending on food services was 11% higher in 2023 than in 2019. So simply returning to pre-pandemic employment levels is not enough to meet demand, unless employees can be 11% more productive.